A few months ago, a buyer in Asia asked me a question I have heard in one form or another for most of my twenty-four years in this industry. “Kolawole,” he said, “why does Nigeria keep selling the ore and buying back the value?” It was not an accusation. It was the polite frustration of a man who understood exactly what he was looking at. We were talking about lithium, the metal that quietly powers almost every phone, laptop, and electric vehicle now rolling off assembly lines across the world, and he could not understand why a country sitting on rich pegmatite belts was content to ship raw rock abroad while others did the profitable work of refining it.

I have thought about that question a great deal since. And the honest answer is that, for a long time, we were content. But that is changing, and faster than most people outside the sector realise. The Lithium Processing Opportunities in Nigeria that exist today did not exist five years ago, and the window that is opening will not stay open forever. So let me walk you through what I see, from the perspective of someone who trades these minerals for a living rather than someone writing about them from a distance.

Why Lithium, and Why Now

Lithium is no longer a niche industrial input. It is the backbone of the global energy transition, and the numbers tell that story plainly. After a punishing slump, prices roared back at the start of 2026. Battery-grade lithium carbonate nearly doubled in the first quarter of the year, with benchmark assessments pushing well above twenty thousand US dollars per metric tonne, and spodumene concentrate climbed back above two thousand dollars per tonne for the first time since late 2023. Analysts at major banks have revised their forecasts sharply upward, citing a widening supply deficit and relentless demand from electric vehicles and grid-scale energy storage.

What makes this matter for Nigeria is not just the price of the raw material. It is the gap between what raw ore earns and what processed lithium chemicals command. Raw spodumene trades in the range of one to two thousand dollars per tonne. Lithium carbonate, the refined chemical that actually goes into batteries, sells for many multiples of that, and lithium hydroxide, preferred for certain high-performance battery chemistries, commands more still. The value added through processing can exceed fifteen hundred percent. For decades, almost all of that value has accrued elsewhere, with a single country controlling roughly seventy percent of the world’s lithium processing capacity. That is the imbalance my Asian buyer was pointing at. And it is precisely the imbalance that creates the opportunity.

What Is Actually Happening on the Ground

This is where I become genuinely optimistic, because for the first time in my career the conversation has moved from intention to construction. Nigeria has committed more than one and a half billion US dollars to lithium and rare earth processing projects, and these are not press-release fantasies. There is a six hundred million dollar lithium processing plant in Nasarawa State that has been reported as ready for commissioning. There is a two hundred million dollar facility near Abuja, and another major plant slated for the Kaduna and Niger State axis. The Africa Finance Corporation, together with the Solid Minerals Development Fund, has anchored a landmark investment to de-risk the sector and pull private capital in behind it.

The federal government, under Solid Minerals Minister Dele Alake, has been explicit about the strategy: process at least thirty percent of our minerals locally, ban or heavily discourage the export of raw ore, and demand beneficiation before anything leaves the country. International players are responding. A large-scale deposit spanning hundreds of square kilometres is being developed with foreign technology partners who intend to build high-purity lithium carbonate capacity on Nigerian soil rather than simply digging and shipping. Analysts have floated projections that the sector’s revenues could climb into the billions over the coming decade. I treat such forecasts with the caution they deserve, but the direction of travel is unmistakable.

Where the Real Opportunities Sit

When people hear “lithium processing,” they immediately picture a billion-dollar refinery, and they assume the opportunity belongs only to sovereign wealth funds and multinational miners. That is a mistake. The processing value chain has many rungs, and several of them are within reach of disciplined Nigerian operators and the partners who back them.

The first opportunity is in upstream concentration and beneficiation. Before lithium ore becomes a battery chemical, it must be upgraded into spodumene concentrate, typically to a six percent lithium oxide grade. This intermediate step is far less capital-intensive than a full chemical conversion plant, yet it multiplies the value of run-of-mine ore substantially and produces exactly the feedstock that both domestic plants and international buyers want. For aggregators and mine-gate operators, this is the most accessible entry point.

The second is in supplying and feeding the new conversion plants. The processing facilities being built will have enormous appetites for consistent, well-characterised concentrate. A plant rated at tens of thousands of tonnes a year cannot run on sporadic, irregular deliveries from disorganised artisanal sources. Whoever can aggregate reliable, quality-controlled feedstock and deliver it on schedule will hold a valuable position in that supply chain. This is precisely the kind of intermediation work that experienced trading and facilitation firms are built for.

The third is in chemical conversion itself, producing lithium carbonate and lithium hydroxide. This is the high-value summit, requiring serious capital, technical partners, reliable power, and patience. It is not for everyone, but for well-structured consortia with international technology partners, it is where the largest margins live and where Nigeria most needs to build.

The fourth, and the one I find most exciting for the long term, is downstream integration toward cathode materials and battery components. This is still nascent, but the government’s stated ambition to become a hub for EV battery manufacturing means the groundwork being laid now will compound for those positioned early.

The Honest Challenges

I would be doing you a disservice if I painted only the bright picture, because anyone who has actually moved tonnes across this terrain knows the obstacles are real. I have lived them.

Power is the first and most stubborn. Lithium chemical conversion is energy-hungry, and Nigeria’s grid generates only a few thousand megawatts for a population north of two hundred million. Any serious processing operation must plan for its own captive power, which adds cost and complexity that investors must price in honestly.

Feedstock organisation is the second. Much of our mining remains informal, artisanal, and undocumented. Plants need predictable volumes of known grade, and bridging the gap between scattered small-scale production and industrial-scale intake is a genuine logistical and trust-building challenge. It is solvable, but it requires people on the ground who understand both the miners and the buyers.

Capital and patience form the third. Processing infrastructure is expensive and slow to build, and lithium prices are notoriously cyclical. The investor who panics at the next downturn will lose; the one who understands that this is a decade-long structural shift will win. Add to this the familiar frictions of regulatory clarity, transparent licensing, infrastructure beyond power, and the need for credible environmental and community stewardship, and you have a sector that rewards seriousness and punishes shortcuts.

None of these challenges cancel the opportunity. They simply define who is equipped to capture it.

Where Augustina Impex Fits In

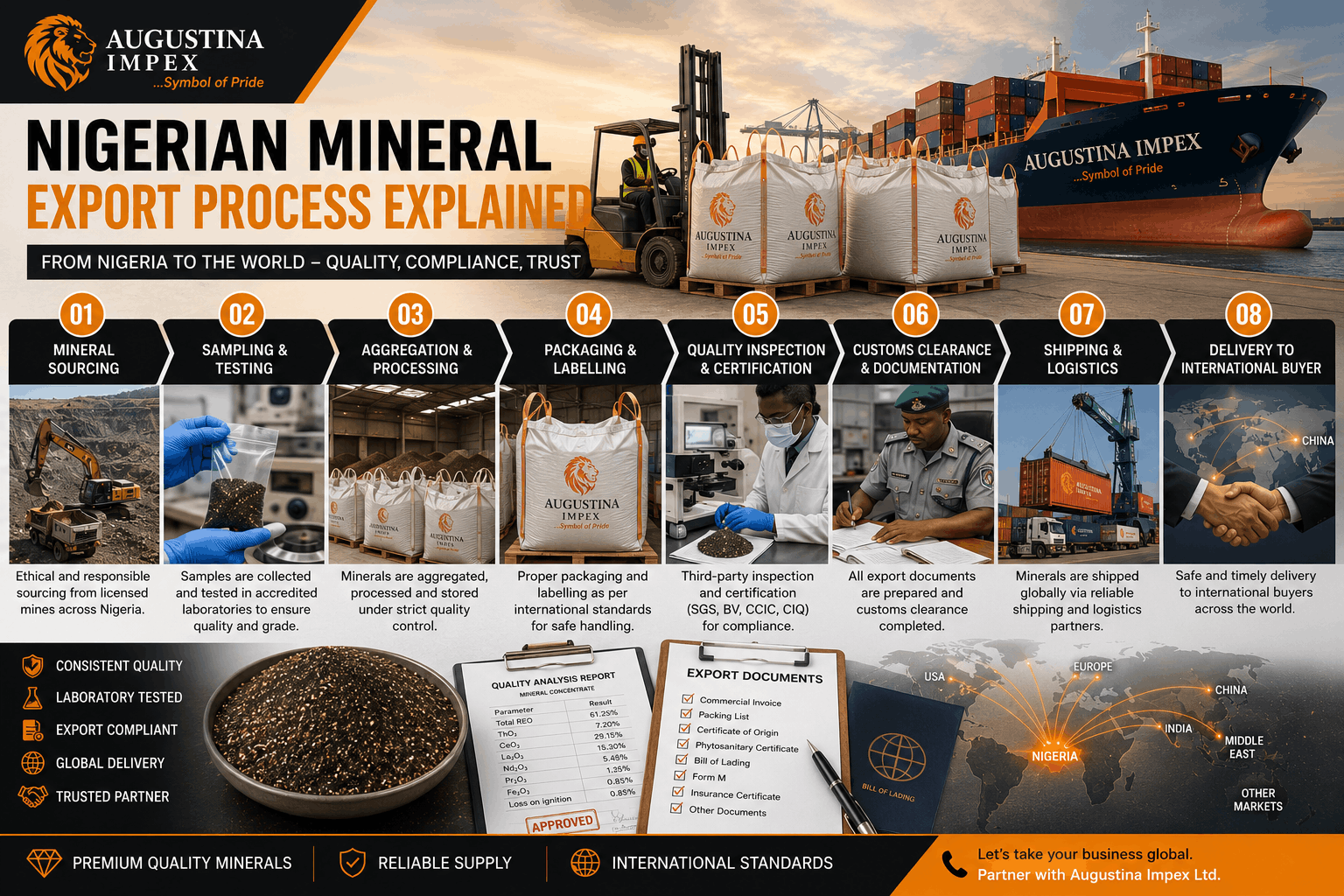

I did not write this to theorise. I wrote it because this is the work my company actually does. At Augustina Impex Limited, we have spent more than two decades trading and facilitating the export of Nigeria’s solid minerals, from tin, columbite, and tantalite to monazite, ilmenite, zircon, and lithium. We understand the gap between a heap of ore at the mine gate and a quality-controlled consignment that an international plant or buyer will actually pay a premium for, because closing that gap is precisely what we do.

For investors and processors, we offer the on-the-ground intelligence, sourcing networks, and export facilitation that turn a strategy deck into shipped tonnes. For miners and aggregators, we provide a credible route to market and the discipline of buyers who demand consistency. As Nigeria’s processing capacity comes online, the firms that can reliably connect feedstock, facilitate transactions, and shepherd consignments through to the buyer will be indispensable, and that is the role we are built to play.

If you are exploring the Lithium Processing Opportunities in Nigeria, whether as an investor seeking entry, a processor needing reliable feedstock, or a buyer wanting a trustworthy partner on the Nigerian side, I would welcome a conversation. The window is open. The question is who moves while it is.

Kolawole King Chief Executive Officer, Augustina Impex Limited #288 Diye Ward, Zarmaganda, Jos South, Plateau State, Nigeria Email: augustinaimpex@gmail.com WhatsApp: +234 906 090 4274 Website: https://augustinaimpex.com Blog: https://augustinaimpexng.blogspot.com/ Advert Video: https://www.youtube.com/watch?v=Izg0t7By6co

#LithiumProcessing #NigeriaLithium #LithiumCarbonate #Spodumene #CriticalMinerals #EVBatteries #MineralBeneficiation #SolidMineralsNigeria #LithiumMining #BatteryMetals #NigeriaMining #LithiumInvestment #ValueAddition #GreenEnergyMinerals #LithiumHydroxide #AfricaLithium #NasarawaLithium #MineralExportNigeria #AugustinaImpex #EnergyTransition #LithiumBoom #SolidMinerals #MiningInvestment

-

Previous Post

How to Invest in the Nigerian Mining Sector

Post a comment

Related Posts

Nigerian Mineral Export Process Explained

If you are buying minerals from Nigeria — whether you are sourcing spodumene concentrate, monazite…

Trusted Monazite Supplier for International Buyers

When international buyers search for a trusted monazite supplier, they are looking for more than…

Why International Buyers Choose Nigerian Lithium Ore

The global race for lithium is intensifying, and a growing number of international buyers —…

Buying Spodumene Concentrate from Nigeria: Complete Import Guide

If you are looking to buy spodumene concentrate from Nigeria, you are positioning yourself at…